A Complete Guide to Business Taxes in Turkey (2025 Update)

18.09.2025

Diving into the Turkish market is an exciting venture, but it comes with a new set of rules—especially when it comes to taxes. At its core, Turkey’s business tax system rests on three main pillars: Corporate Income Tax on your profits, Value Added Tax (VAT) on sales, and withholding taxes on certain payments you make.

Getting a handle on these isn’t just about compliance; it’s about understanding the financial landscape you’re operating in. Think of it as learning the local ground rules to play the game effectively.

Understanding corporate tax, VAT, and withholding taxes in Turkey

Let’s be honest, tackling a new tax system can feel overwhelming. The terminology is different, the deadlines are unfamiliar, and the last thing you want is a misstep. This guide is here to cut through the jargon and give you a clear, practical overview of business taxes in Turkey. The system itself is actually quite logical, designed to fund the country while still encouraging businesses like yours to invest and grow.

Simplify your business setup with Workon’s all-in-one company registration service in Turkey.

To make sense of it all, I find it helpful to think of the tax system as a financial toolkit. Each tax is a different tool for a specific job:

Corporate Income Tax (CIT): This is the big one—the tax on your company’s net profits.

Value Added Tax (KDV): A consumption tax added at every stage of the supply chain, which the final customer ultimately pays.

Withholding Tax (Stopaj): Think of this as a pre-payment of tax, collected at the source on things like dividends, royalties, and fees for professional services.

These pieces all work together, and once you understand how they fit, managing your financial obligations becomes much more straightforward.

Understanding the Core Components

Seeing the main taxes laid out side-by-side helps clarify their purpose. Each one targets a different part of your business activity, from the money you make to the goods you sell. This is a pretty standard approach you’ll find in many countries. And as more companies embrace flexible work arrangements, getting familiar with the basics of remote work taxes is also a smart move for any modern business.

The Turkish tax system is comprehensive, covering income, consumption, and wealth. For businesses, the key is to understand how corporate tax, VAT, and withholding taxes interact within their specific operational model.

To give you a quick snapshot, the table below breaks down the essential business taxes. This is your at-a-glance guide to the main rates and what they apply to.

Quick Overview of Key Business Taxes in Turkey

Here’s a simple summary of the main taxes your business will encounter in Turkey.

Tax Type

Standard Rate

Tax Base

Corporate Income Tax

25%

Company’s net profit after deductions

Value Added Tax (VAT)

20% (Standard)

The value of goods and services supplied

Withholding Tax (WHT)

Varies (e.g., 10% on dividends)

Gross amount of payments like dividends, interest, royalties

This table provides a great starting point. For a more detailed breakdown and further valuable insights, be sure to check out our complete guide on https://workon.com.tr/en/taxes-in-turkey/.

Getting to Grips with Corporate Income Tax in Turkey

If you’re doing business in Turkey, the Corporate Income Tax (CIT) will be your most significant financial consideration. It’s the main tax applied to your company’s net profits, and getting your head around it is absolutely fundamental to smart financial planning. This isn’t just about a number; it’s about understanding the journey from revenue to tax liability.

Whether you’re a local entrepreneur or a branch of a global giant, the principle is straightforward. The government taxes the profit your business makes after you’ve subtracted all your legitimate operating costs. Think of it as an orchard: you only pay tax on the fruit you actually sell, not the entire harvest, once you’ve accounted for the costs of water, fertiliser, and paying your workers.

How to Calculate Your Taxable Profit

Figuring out your taxable profit is a game of careful subtraction. The Turkish tax system allows businesses to deduct a whole host of expenses that were necessary to generate income. This makes sure you’re taxed fairly on what you actually earned, not just what you sold.

Here are some of the most common things you can deduct:

Day-to-Day Operations: This is the big stuff—employee salaries, office rent, and utility bills.

Sales and Marketing Costs: Any money you’ve spent on advertising, paying sales commissions, or other promotional efforts is usually deductible.

Asset Depreciation: Big-ticket items like machinery or company vehicles lose value over time. You can write off this cost over their useful lifespan.

Interest and Royalties: If you’re paying interest on a business loan or royalties for using intellectual property, those payments can typically be deducted.

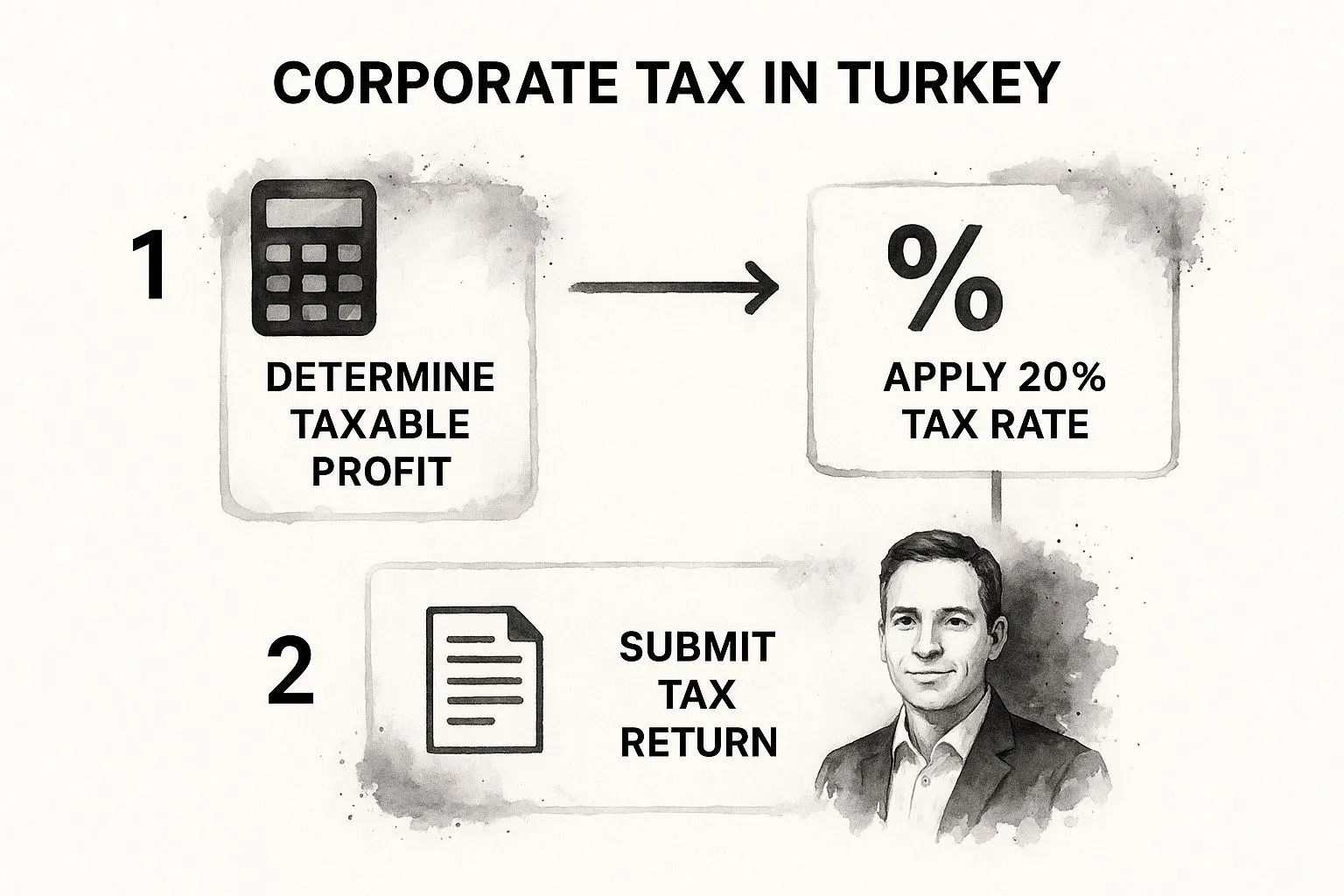

By keeping a close eye on these deductions, you can accurately nail down your net profit, which is the starting block for calculating your corporate tax. The visual below breaks down the key steps involved.

A simple guide to determining taxable profit and filing corporate tax returns in Turkey

As the infographic shows, it’s a structured process. You move step-by-step from working out your profit to applying the right rate and, finally, filing your return.

The Standard and Minimum Tax Rules Explained

Turkey has a pretty unique dual-track system for corporate tax, which is designed to keep things fair while ensuring a stable tax base. The standard corporate tax rate is a flat 25% for most companies, and this applies to everyone, including foreign-owned businesses. It’s worth noting that financial institutions like banks have their own, higher rate of 30%.

But there’s a twist you need to know about: the minimum tax rule. This acts as a sort of safety net for the government, stopping companies from using a mountain of deductions to wipe out their tax bill completely.

The minimum tax rule forces companies to calculate a separate tax based on 10% of their income before certain major deductions and exemptions are applied. Your final tax payment is whichever of the two calculations is higher—the standard 25% CIT on your net profit or the 10% minimum tax.

This means that when tax season rolls around, you have to do two sets of sums. Let’s say your standard 25% calculation gives you a tax bill of ₺80,000. But when you run the numbers for the 10% minimum tax, it comes out to ₺95,000. In that scenario, you are legally required to pay the higher amount: ₺95,000. For a deeper dive with more examples, check out our detailed guide on the 2025 Corporate Tax rates and minimum tax rule.

Some types of income, like dividends from other Turkish companies or profits from approved R&D projects, don’t count towards this minimum tax base. This two-pronged system ensures every business contributes a baseline amount while still offering tax breaks for activities the government wants to encourage. To stay compliant and plan effectively, you really need to master both calculations.

Navigating Your VAT Obligations

Understanding Value Added Tax for Businesses

Value Added Tax, or as it’s known locally, Katma Değer Vergisi (KDV), is a part of almost every business transaction in Turkey. At first glance, it can seem a bit intimidating, but the core idea is actually quite straightforward.

Think of your business as a temporary custodian for the tax authorities. You collect KDV from your customers on their behalf and then pass it along to the government, but not before you subtract the KDV you’ve already paid on your own business expenses. It’s the end consumer who ultimately bears the cost; for you, it’s all about diligent administration. Getting this flow right is the key to mastering your obligations and avoiding any unpleasant surprises.

Understanding VAT Rates and Categories

In Turkey, not everything is taxed at the same rate. The government uses a tiered system for KDV, applying different rates to balance revenue needs with economic priorities. This approach makes essential items more affordable while placing a higher tax on non-essential or luxury goods.

Because of this tiered structure, you have to be absolutely sure which rate applies to your specific products or services. Applying the wrong one is a surprisingly common mistake and can cause major headaches if the tax authorities come knocking.

Here’s a quick rundown of the main KDV rates you’ll work with:

Standard Rate (20%): This is the default and most common rate. It applies to most goods and services that don’t qualify for one of the reduced rates.

Reduced Rate (10%): You’ll generally find this rate on basic foodstuffs, textiles, and a handful of other essential items.

Super-Reduced Rate (1%): This lowest rate is reserved for a very specific list of goods, like certain agricultural products, newspapers, and magazines.

Correctly categorising every sale is essential for accurate filing. For a deeper dive into what falls where, you can learn more about VAT rates and compliance in Turkey to make sure your business is perfectly aligned.

Calculating Your Net VAT Liability

The real heart of managing your KDV lies in a simple calculation that determines what you owe the tax office each month. It’s a balancing act between the tax you’ve collected and the tax you’ve paid.

The whole process boils down to two key figures:

Output VAT: This is the tax you charge your customers on your invoices when you sell your products or services.

Input VAT: This is the tax you pay on your own business purchases—things like raw materials, office supplies, or professional services.

Your net VAT payment is simply the difference between what you collected and what you paid.

VAT Calculation Formula: Net VAT Payable = Total Output VAT (Collected on Sales) – Total Input VAT (Paid on Purchases)

Let’s walk through a quick example. Imagine you run a business selling handmade ceramics. In one month, you collect ₺20,000 in VAT from your customers (your Output VAT). In that same period, you paid ₺8,000 in VAT on supplies like clay, glaze, and electricity for the kiln (your Input VAT).

The calculation is straightforward: ₺20,000 – ₺8,000 = ₺12,000. That ₺12,000 is the amount you need to send to the tax office for that month. On the off chance your Input VAT is more than your Output VAT, you can usually carry that credit forward to reduce your bill in the following months.

Filing and Payment Procedures

When it comes to Turkish business taxes, deadlines are not suggestions. For VAT, everything runs on a monthly cycle. You must file your VAT return for the previous month by the 28th day of the current month, and any tax you owe must be paid by that same date.

All filings are handled electronically through the Turkish Revenue Administration’s online portal. This digital process means keeping organised, accurate records of every single sale and purchase isn’t just good practice—it’s a legal necessity. Your invoices are your proof for claiming back Input VAT, so think of meticulous record-keeping as your best defence against compliance problems.

Understanding Withholding and Other Key Taxes

Once you’ve got your head around corporate tax and VAT, you’ll find a few other levies on the Turkish tax landscape. To get the full picture of your company’s obligations, you need to be familiar with these, starting with one of the most common: withholding tax.

Locally, this is known as stopaj, and it’s basically a tax payment made at the source of a transaction. Instead of waiting for the person receiving the money to pay their tax down the line, the company making the payment simply holds back a percentage and sends it straight to the tax authorities. It’s a smart way for the government to ensure taxes are collected promptly on certain types of income.

The easiest way to think of it is like the PAYE system for an employee’s salary, but applied to payments between businesses or from a business to an individual. It’s a core part of the tax system here and pops up in all sorts of common domestic and international transactions.

How Withholding Tax Works in Practice

So, when does this actually apply to you? If your company is making certain kinds of payments—like for professional services or when distributing profits—you’re on the hook for calculating, withholding, and paying the tax.

You’ll commonly see stopaj applied to payments like:

Dividends: When profits are paid out to shareholders.

Royalties: Payments for using intellectual property, such as patents or brand names.

Professional Service Fees: Invoices from self-employed professionals like lawyers, accountants, or consultants.

Rental Payments: When leasing commercial property from an individual landlord.

The rates aren’t one-size-fits-all; they change depending on what’s being paid for. For example, dividends paid to non-resident shareholders are a classic case where withholding tax comes into play, acting as a key lever in Turkey’s fiscal policy.

For anyone doing business internationally, getting these rates right is essential. The good news is that Turkey has an extensive network of double taxation treaties that can dramatically reduce the standard rates, making the investment climate much more attractive.

This really shows how Turkey’s tax policy is constantly adapting to balance domestic needs with global economic realities. Just look at the corporate tax rate over the years—it’s a perfect example. Between 1997 and today, the rate has averaged around 24.52%, swinging from a high of 33% in 2000 to a low of 20% in 2006. This history gives you crucial context for understanding the current tax framework. For a closer look at these shifts, you can find more insights about tax rates in Turkey on ozbekcpa.com.

Exploring Other Important Business Levies

A truly complete view of business taxes in Turkey means looking past withholding tax. Depending on your industry and what you sell, you might run into a few other specific taxes.

These aren’t as universal as corporate tax but are targeted at particular sectors or products. Knowing if they apply to you is key for solid financial planning and staying out of trouble with the tax office.

Special Consumption Tax (ÖTV)

The Special Consumption Tax (ÖTV) is a one-off tax charged on a specific list of goods, usually when they’re first manufactured or imported. It doesn’t get passed down the supply chain. The goods that fall under ÖTV are grouped into four main buckets:

Petroleum products, natural gas, and various oils.

Motor vehicles, from cars to motorcycles and yachts.

Alcoholic drinks and tobacco products.

Luxury items like furs, caviar, and high-end electronics.

The ÖTV rates can be very high, especially on things like cars and luxury goods, so it’s a huge cost factor for any business dealing in these products.

Banking and Insurance Transaction Tax (BITT)

This tax, or Banka ve Sigorta Muameleleri Vergisi (BSMV), is aimed squarely at the financial sector. It applies to transactions and services from banks and insurance companies. If you’re in this field, BSMV is a major part of your tax world, effectively replacing VAT for most of what you do.

Digital Services Tax (DST)

Keeping up with global trends, Turkey rolled out a Digital Services Tax (DST). This tax is for the big players in the digital world that earn significant revenue from users in Turkey. It applies to income from online advertising, digital content sales, and services that connect users on a platform. The current rate is 7.5%, charged on the gross revenue these companies generate in Turkey.

Meeting Deadlines and Tax Compliance Procedures

Ensuring Timely Submissions for Business Success

Getting a handle on the different business taxes in Turkey is one thing, but staying compliant is where the real work begins. It’s a constant loop of tracking, filing, and paying that requires a sharp eye on the calendar and a well-organised approach.

Think of tax compliance as the routine maintenance that keeps your company’s financial engine humming. If you skip a service, you’re risking a costly breakdown—penalties, interest charges, and a lot of unwanted attention from the tax authorities. By setting up a solid rhythm for your tax duties, you can keep things running smoothly and sidestep these entirely preventable headaches.

The core of meeting your obligations is simple: know what to file and when to file it. The good news is that Turkey’s tax year for businesses lines up neatly with the calendar year, running from January 1st to December 31st. This makes planning a bit more straightforward. The key is to map out your deadlines well in advance.

Key Tax Filing and Payment Deadlines in Turkey

To help you keep everything straight, here’s a schedule of the most important tax deadlines for businesses to follow throughout the year. These are the dates you absolutely need to have circled in red on your calendar to ensure compliance.

Tax Type

Filing Frequency

General Deadline

Corporate Income Tax (CIT)

Annually

Filed by the end of April of the following year.

VAT (KDV)

Monthly

Filed and paid by the 28th of the following month.

Withholding Tax (Stopaj)

Monthly or Quarterly

Filed and paid by the 26th of the following month.

While public holidays can sometimes cause minor shifts, this table gives you a reliable roadmap for your year-round tax activities. Missing these dates can trigger immediate financial penalties, so treat them as non-negotiable.

Embracing Digital Tax Administration

Turkey has really pushed its tax system into the modern era, moving nearly every process online. This shift makes filing much easier, but it also means businesses need to get comfortable with the official digital platforms. The main hub for everything tax-related is the Interactive Tax Office (İnteraktif Vergi Dairesi).

This is your one-stop online portal for managing almost all of your tax duties. Through this system, you can:

Submit your CIT, VAT, and withholding tax returns.

Make secure tax payments.

Check your tax records and see past filings.

Communicate officially with the tax authorities.

This digital-first system makes meticulous record-keeping more important than ever. Every single transaction, invoice, and expense needs to be recorded accurately because this data is the foundation of your electronic filings. To keep everything in order, many businesses use efficient tax preparation solutions to manage the complexity and ensure accuracy.

The backbone of stress-free tax compliance is diligent and organised record-keeping. Your digital and physical records are your primary evidence in the event of a query or audit from the Turkish Revenue Administration.

Ultimately, staying on top of your taxes in Turkey comes down to a mix of calendar discipline and digital know-how. By mastering the deadlines and getting comfortable with the online tools, you can confidently meet your obligations and focus on what really matters: growing your business.

Unlocking Turkey’s Generous Tax Incentives

Paying taxes is a given, but paying more than you have to isn’t. The Turkish government has rolled out a fantastic range of tax incentives designed to attract investment into specific industries and regions. These aren’t just small breaks; they’re serious, substantial benefits that can dramatically lower what you owe and inject cash back into your business.

When you know how to use these programmes, you can stop seeing tax as just another business cost. Instead, it becomes a tool to sharpen your competitive edge. The trick is simply knowing where to look and what it takes to qualify, especially if your business is in innovation or exports.

The Power of Technology Development Zones

Turkey’s Technology Development Zones, often called Teknoparks, are special hubs created to foster innovation. To encourage companies to set up shop here, the government offers some pretty incredible tax breaks. Essentially, they’ve created protected areas where the normal tax rules don’t fully apply, all to fuel research, software development, and high-tech production.

If your company’s activities fit the bill, the advantages are huge:

Zero Corporate Income Tax: Any profits you make from software development, R&D, and design work inside the zone are 100% exempt from corporate income tax right through to the end of 2028.

VAT Exemption: When you sell software or other digital products created within the Teknopark, you don’t have to charge VAT.

Payroll Support: Your R&D, design, and support staff won’t pay any income tax on their salaries. On top of that, the government will cover 50% of the employer’s social security contribution for the first five years.

Getting an Edge in the Free Zones

Beyond the Teknoparks, Turkey has also set up Free Zones near its major ports and trade hubs. These are all about boosting export-focused businesses. They offer a much friendlier tax and regulatory climate, making them a perfect base for companies that manufacture goods for international markets or engage in global trade.

Being based in a Free Zone comes with its own unique set of perks that can seriously cut your operating costs and improve your bottom line.

For manufacturing companies, the headline benefit is a 100% exemption from corporate income tax on all earnings from their production activities. This is a key part of Turkey’s strategy to pull in foreign investment and build its export economy.

But that’s not all. Businesses in these zones are also completely exempt from VAT and customs duties for any goods they import from abroad. And if your company exports at least 85% of what it produces, your employees’ salaries are exempt from income tax, too.

Making the Most of R&D and Design Incentives

What if your business isn’t located in a Teknopark or a Free Zone? Don’t worry, you can still tap into some powerful incentives for your Research & Development (R&D) and design work. The government allows you to deduct 100% of your qualifying R&D and design spending straight from your taxable profit.

This covers a wide range of expenses, including staff wages, materials, and even fees for outside consultants. As long as you keep good records of your innovation projects, you can significantly lower your corporate tax bill while simultaneously investing in the future of your company.

Frequently Asked Questions

Getting to grips with Turkish business taxes can feel like a maze, especially if you’re juggling different company types or international operations. Let’s break down some of the most common questions business owners have with clear, straightforward answers.

What’s the Real Tax Difference Between an LTD and an A.Ş. Company?

On the surface, there’s not much of a difference. When it comes to the main corporate income tax, both Limited Liability Companies (LTD) and Joint-Stock Companies (A.Ş.) pay the same standard 25% rate on their yearly profits. They’re on a level playing field there.

The important distinctions really pop up in areas like corporate governance and shareholder liability, not the tax rate itself. These factors can indirectly shape your tax planning, especially when you start thinking about how to distribute profits and handle dividend withholding tax. But for the day-to-day grind of CIT and VAT filings, you’ll find their obligations are virtually identical.

How Do Double Taxation Treaties Affect My Business?

If you’re running an international business with a footprint in Turkey, Double Taxation Treaties (DTTs) are your best friend. Turkey has these agreements with over 85 countries for one simple reason: to stop your income from being taxed twice, once in Turkey and again back home.

Think of it this way: a DTT can slash the standard 10% withholding tax on dividends you send from your Turkish company to a foreign shareholder. The actual reduced rate depends on the specific treaty with that country, so it’s always worth checking the fine print to see how much you can save.

What Happens If I Miss a Tax Deadline?

Miss a tax deadline in Turkey, and you’ll feel the sting pretty quickly. The authorities don’t just charge a penalty for filing late; they also add late payment interest, which clocks up for every single day the tax remains unpaid.

The interest rate itself is set by the government and changes from time to time based on the economy. What’s more concerning is that consistent delays can put a huge target on your back for a full tax audit. An audit is a demanding, time-sucking process, so staying on top of your deadlines is always the smartest move.

Navigating Turkish tax law requires an expert touch. Workon specialises in helping businesses set up and run their operations in Turkey, making sure you stay compliant so you can focus on growth. Let our team of professionals handle the complexities for you. Find out more at https://workon.com.tr/en.

The key taxes are Corporate Income Tax (25%), Value Added Tax (20% standard rate), and Withholding Tax on payments like dividends, royalties, and services.

The standard corporate income tax rate is 25%, with a higher 30% rate for financial institutions. A minimum tax rule also applies in certain cases.

VAT in Turkey has three levels: 20% standard rate, 10% reduced rate for essentials like food, and 1% super-reduced rate for certain agricultural products and media.

Dividends are subject to withholding tax, typically 10%. However, Double Taxation Treaties may reduce this rate depending on the shareholder’s country.

Yes. Technology Development Zones, Free Zones, and R&D incentives offer major exemptions, including corporate tax breaks, VAT exemptions, and payroll support.

Subscribe to Newsletter

Be notified of the latest news in the business world quickly