Bookkeeping in Turkey for Small Businesses: Legal, Tax, and Software Guide (2025 Update)

06.10.2025

So, you’re starting a business in Turkey. It’s an exciting time, but navigating the local financial landscape is crucial. Good bookkeeping in Turkey for small businesses isn’t just about tracking numbers; it’s about choosing the right legal structure from the very beginning and staying on top of mandatory reporting. This is your foundation for avoiding stiff penalties and setting yourself up for real, sustainable growth.

In Turkey, getting your financial house in order from day one isn’t optional—it’s essential. The first big decision you’ll make is choosing a business structure. This choice will shape everything that follows: your bookkeeping duties, your tax burden, and your legal responsibilities. Think of it as the financial blueprint for your entire company.

For most small businesses, the decision boils down to two main options: a sole proprietorship (şahıs şirketi) or a Limited Liability Company, commonly known as an LLC (limited şirket). They might sound similar, but when it comes to bookkeeping, they are worlds apart.

Sole Proprietorship vs LLC Key Differences

The sole proprietorship is the go-to for many freelancers and solo entrepreneurs because it’s easier to set up and run. The bookkeeping is generally more straightforward, relying on a single-entry system recorded in an operating ledger (işletme defteri). This method simply tracks your income and expenses as they happen.

An LLC, however, is a separate legal entity from its owners. This distinction demands a more formal, double-entry bookkeeping system. You’ll be legally required to maintain several commercial books, such as a journal (yevmiye defteri), a general ledger (defter-i kebir), and an inventory book (envanter defteri). While this means more work, the trade-off is significant liability protection.

The core takeaway is this: your choice of business entity dictates the complexity of your financial records. An LLC provides a corporate veil but requires meticulous, legally mandated bookkeeping, whereas a sole proprietorship is simpler but intertwines business and personal liability more closely.

Initial Registration is a Critical Step

No matter which structure you land on, your very next stop is the Turkish Revenue Administration (GİB – Gelir İdaresi Başkanlığı) for registration. This isn’t just red tape; it’s the official step that puts your business on the government’s radar for all tax and reporting matters. Here, you’ll get your tax identification number, a non-negotiable for any commercial activity in Turkey.

Once registered, your tax obligations kick in, especially for Value Added Tax (KDV). From that moment on, every single transaction must be recorded and every invoice issued according to Turkish law. This is also the perfect time to open a dedicated business bank account to keep your personal and company finances separate, which is a lifesaver come tax time. For a deeper dive into this process, check out our guide on how to open a business bank account in Turkey.

With your records in order, you can start using that data to make smart decisions. Understanding key business analysis best practices can help you transform raw financial data into a roadmap for growth. Well-kept books are your single source of truth, helping you nail everything from pricing strategies to expansion plans. Getting this foundational stage right turns bookkeeping from a legal chore into one of your most powerful business tools.

Mastering Turkish Bookkeeping and Tax Rules

A practical guide for small business owners navigating Turkey’s accounting and tax system.

When you’re running a small business in Turkey, getting your bookkeeping right isn’t just good practice—it’s everything. The rules are strict, and the authorities demand precision. A simple misunderstanding of local requirements can lead to heavy penalties that could seriously damage an otherwise healthy business. It all begins with knowing which records you are legally required to keep.

The foundation for all this is built on two key pieces of legislation: the Turkish Commercial Code (TTK) and the Tax Procedure Law (VUK). These aren’t just suggestions; they lay down the law for how you must record every financial move your business makes. They mandate specific commercial books that create the official, chronological history of your company’s finances.

Your Legally Required Commercial Books

If you’re operating as a limited liability company (LLC), there are two books that are absolutely essential:

The Journal (Yevmiye Defteri): This is your day-to-day financial diary. Every single transaction, from a major client payment to buying office coffee, gets recorded here first, in chronological order. Crucially, each entry needs a supporting document, like an invoice or receipt, and must be logged within ten days of the transaction.

The General Ledger (Defter-i Kebir): Think of this as the organised version of your journal. It takes all that raw, chronological data from the yevmiye defteri and neatly sorts it into different accounts—cash, receivables, sales revenue, and so on. This gives you a clear, structured overview of where your money is.

These two books are the bedrock of your official financial statements. They are also the very first thing a tax inspector will demand to see in an audit. Keeping them perfectly accurate and up-to-date isn’t just a chore; it’s a legal necessity.

A common pitfall I see with new entrepreneurs is treating these books like a year-end task. That’s a mistake. They need to be maintained in real-time. Accurate, timely entries are your best defence in an audit and, just as importantly, give you a live pulse on your company’s financial health.

Simplify your business setup with Workon’s all-in-one company registration service in Turkey.

Navigating Key Business Taxes

Keeping your books in order is one half of the equation; understanding the tax landscape is the other. For most small businesses in Turkey, you’ll be dealing with three main taxes on a regular basis, each with its own deadlines and rules. For a deep dive, you can check out our comprehensive guide on business taxes in Turkey.

Here’s a quick rundown of what you need to keep on your radar:

Value Added Tax (KDV): This is a consumption tax added to most goods and services, with standard rates usually sitting at 1%, 10%, or 20%. You’ll collect KDV from your customers, subtract the KDV you’ve paid on your own business expenses, and then declare and pay the difference to the tax office every month.

Income or Corporate Tax: This depends on your business structure. Sole proprietors pay a progressive income tax on their earnings, while LLCs pay a flat corporate tax rate on net profits. While it’s calculated annually, you don’t wait until the end of the year to pay it. Instead, you make advance quarterly payments based on your profit for that period.

Withholding Tax (Stopaj): This is a tax you deduct from certain payments you make to others—for example, from the rent you pay your landlord or from fees paid to a freelance consultant. You are responsible for paying this withheld amount directly to the tax authorities, usually on a quarterly basis.

The Mandatory Shift to Digital Bookkeeping

Turkey has been aggressively moving its entire financial system online through a government initiative called e-dönüşüm, or e-transformation. This programme is making it mandatory for businesses to use digital formats for key financial documents, phasing out the old paper-based methods.

Depending on your annual revenue and industry, you might be required to adopt these systems. The main components you’ll encounter are:

E-Invoice (e-Fatura): Used for all your business-to-business transactions with other companies that are also registered in the e-invoice system.

E-Archive (e-Arşiv): Used for invoices you issue to individual customers or to businesses that aren’t part of the e-fatura system.

E-Ledger (e-Defter): This is the digital submission of your official journal and general ledger directly to the Turkish Revenue Administration (GİB).

This rapid digital shift has pushed many small and medium-sized businesses to seek expert help. It’s a global trend; companies everywhere are outsourcing their bookkeeping to keep up with complex rules. In Turkey, this has created huge demand for cloud-based platforms that can maintain audit-ready digital records. Making this strategic move helps businesses stay on the right side of ever-increasing digital reporting demands. Mastering these rules is your key to operating smoothly and avoiding any unpleasant surprises from the tax office.

Choosing the Right Bookkeeping Software

Find the best accounting software for managing your business finances in Turkey.

Forget about spreadsheets and manual ledgers. In Turkey, trying to manage your books the old-fashioned way is not just inefficient—it’s a recipe for compliance headaches. The right software is more than just a digital file cabinet; it’s your first line of defence against costly mistakes and a massive time-saver.

The demand for small business software here is booming. With around 3.3 million SMEs in the country, the market is expanding quickly. This isn’t just a trend; it’s a direct response to the government’s push for digital transformation and increasingly complex tax rules. A recent report from Strategy& highlights this surge, projecting an incredible 28% CAGR for the sector, which you can read more about on their analysis of the Turkish SME software market.

All this growth means you’ve got plenty of options. But it also means you have to be smart about your choice. Don’t get distracted by flashy marketing—your number one priority must be flawless compliance with Turkish regulations.

Local Champions Versus International Players

As you start looking, you’ll see two types of software: homegrown Turkish solutions and big international names that have added Turkish features. I’ll be blunt: for most small businesses here, the local options are almost always the better bet.

Turkish-developed platforms like Paraşüt, Logo İşbaşı, and MikroX were built from the ground up for the Turkish financial ecosystem. Their entire architecture is designed for one thing: to communicate seamlessly with the Turkish Revenue Administration (GİB).

This native integration is absolutely critical for handling Turkey’s mandatory e-transformation processes, such as:

E-Fatura and E-Arşiv: Creating and sending legally perfect electronic invoices directly through the GİB portal.

Automatic KDV Calculation: Applying the correct Value Added Tax (1%, 10%, or 20%) to every transaction and generating spot-on monthly declarations.

Stopaj (Withholding Tax) Tracking: Correctly managing and reporting withholding taxes on things like freelance payments or rent.

Sure, global giants like QuickBooks or Xero are fantastic tools, but their Turkish features can sometimes feel bolted on rather than built-in. For true peace of mind and smoother day-to-day operations, a dedicated local solution is the most reliable choice for a small business in Turkey.

Key Features You Can’t Ignore

When comparing your options, cut through the noise and focus on the features that actually make your life easier. You’re looking for a tool that makes staying compliant feel automatic.

When you have the right tool, you get immediate financial clarity. Everything is right there on the dashboard—cash flow, upcoming bills, outstanding invoices. It’s an instant health check for your business.

So, what should be on your checklist? Here’s what I tell every new business owner to look for:

Direct GİB Integration: This is non-negotiable. Can the software send e-invoices directly to the GİB without needing a clumsy third-party connector?

Bank Feed Automation: Does it sync automatically with Turkish bank accounts to pull in your transactions? This one feature will save you dozens of hours of manual entry.

Mali Müşavir Access: Your Financial Advisor (Mali Müşavir) needs to access your books to file your official declarations. The software must have a secure, easy way to grant them access.

Scalability: Think about the future. Will the software grow with you? If you hire employees next year, will it handle payroll?

Ease of Use: Is the interface clean and intuitive? If you’re not fluent in Turkish, is there a solid English version? A confusing system just creates more work.

Choosing the right software is a genuine investment in your business’s future. Finding a tool that nails Turkish compliance and automates the grunt work frees you up to focus on what you actually set out to do: run and grow your business.

With so many solid local options, picking the right one comes down to your specific needs. The table below breaks down a few of the market leaders to help you get started.

Comparing Popular Bookkeeping Software in Turkey

Software

Best For

GİB E-Transformation Integration

Pricing Model

Key Feature

Paraşüt

Freelancers and service-based businesses looking for an easy-to-use interface.

Excellent. Direct integration for E-Fatura, E-Arşiv, and E-SMM.

Subscription-based (monthly/annual) with tiered plans.

Superb user experience and strong mobile app functionality.

Logo İşbaşı

Small businesses that anticipate scaling up and needing more advanced features.

Comprehensive. Covers all major e-transformation modules.

Subscription-based. Often bundled with other Logo business products.

Strong inventory management and integration with other Logo ERPs.

MikroX

Startups and micro-businesses that need a cost-effective, cloud-based solution.

Full integration for core GİB requirements.

Freemium and affordable subscription tiers.

Generous free plan for very small businesses just starting.

Bizim Hesab

Retail and e-commerce businesses needing a simple, all-in-one solution.

Strong. Includes E-Fatura, E-Arşiv, and e-commerce integrations.

Tiered subscription model based on transaction volume.

Ultimately, the best software is the one that fits your workflow and gives you confidence that your finances are in order. Most offer free trials, so take them for a spin before you commit.

Building Your Daily, Monthly, and Annual Bookkeeping Rhythm

Good bookkeeping in Turkey isn’t about that mad dash at the end of the year, frantically digging through a shoebox of crumpled receipts. Far from it. The secret is to build a steady rhythm—a simple set of habits that keep your financial records clean, compliant, and actually useful for running your business.

When you break down the work into daily, monthly, and annual tasks, what seems like a mountain becomes a series of manageable steps. This approach takes the chaos out of your finances, ensuring you’re always ready for tax deadlines and have a crystal-clear view of your company’s health at any given moment.

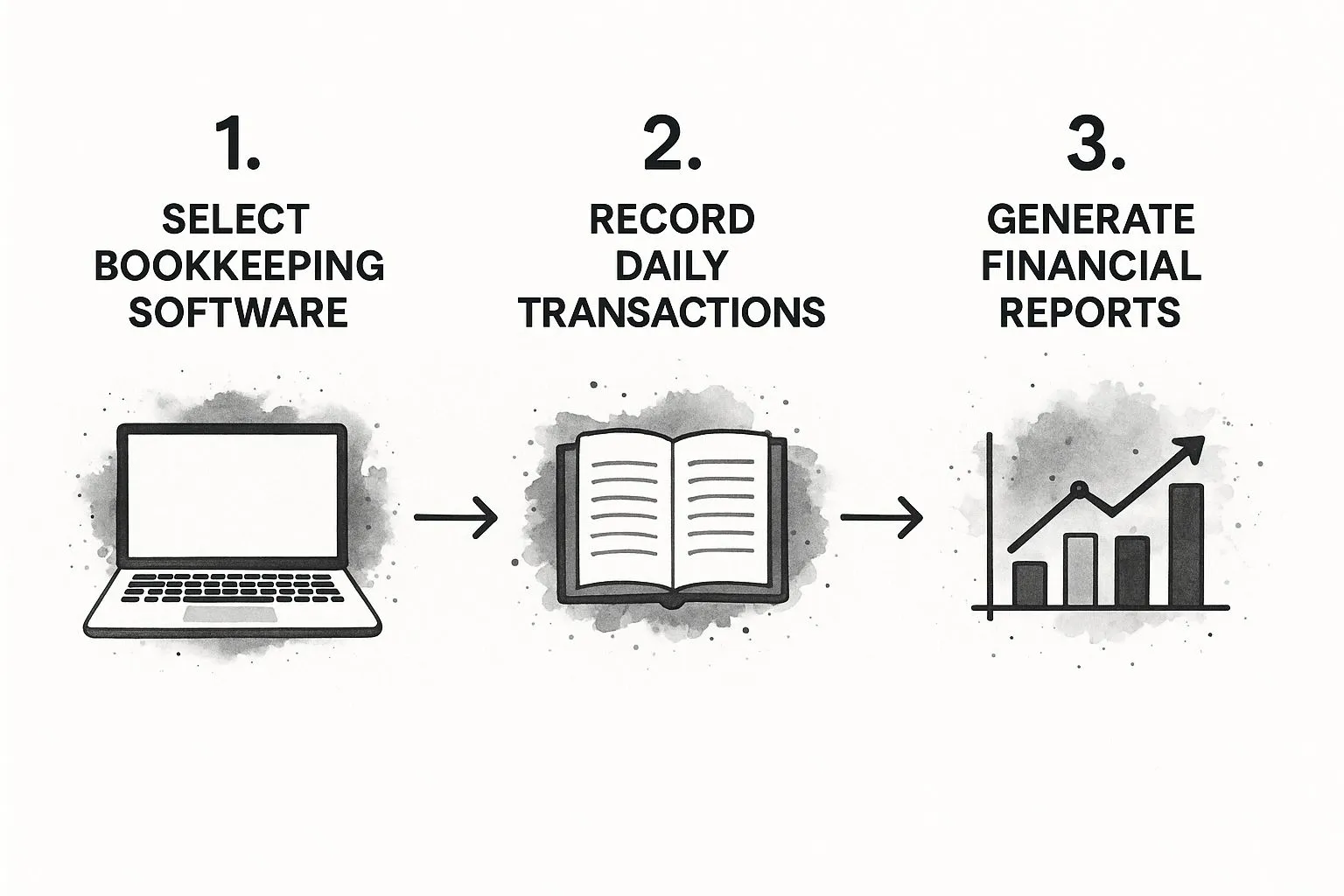

The process is surprisingly straightforward, building from one step to the next, as you can see here.

From software selection to reporting: building daily bookkeeping habits

It really boils down to three core actions: picking the right tools, logging your daily activity without fail, and then using that data to generate reports that tell you the story of your business. That’s the foundation of a bookkeeping system that works for you.

Your Daily Financial Habits

The key to stress-free bookkeeping lies in small, consistent actions. These daily tasks only take a few minutes but are your best defence against small issues spiralling into major headaches. Think of them as non-negotiable parts of your day.

Log Every Transaction, Instantly: Paid a supplier? Got a payment from a client? Get it into your accounting software right away. This single habit is the difference between clarity and a confusing mess at the end of the month.

Issue Invoices Properly: In Turkey, every single sale needs an official invoice. If you’re selling to another business, that means an e-fatura. For individual customers, it’s an e-arşiv. Make it a rule to generate and send these the same day you deliver the product or service.

File Every Document Digitally: That receipt from the office supply store or an invoice from a contractor? Scan it immediately and attach it directly to the transaction in your software. This digital paper trail will be your absolute best friend if you ever face an audit.

Your Monthly Financial Check-Up

Set aside a dedicated block of time at the end of each month to get your financial house in order. This is your moment to catch errors, chase up late payments, and get a true picture of how you performed.

The main job here is to reconcile your accounts. This simply means comparing every transaction in your bookkeeping software against your business bank statements. They have to match, down to the last kuruş. Any discrepancy is a red flag—it could be a missed expense, a double entry, or something more serious.

This is also when you get on top of your cash flow. Pull up your accounts receivable report to see who hasn’t paid you yet and send out polite reminders. On the flip side, check your accounts payable to make sure your own bills are paid on time, keeping your supplier relationships strong.

This monthly review is more than just a box-ticking exercise; it’s a vital strategic checkpoint. It tells you exactly where your money is going and shines a light on potential cash flow problems before they become critical, giving you the chance to act.

Your Annual Financial Wrap-Up

As the fiscal year comes to a close, your attention will shift to finalising your books and gearing up for your annual tax declarations. If you’ve been diligent with your daily and monthly habits, this process will be smooth and straightforward. All that hard work is about to pay off.

Your primary task is to “close the books.” This involves working with your Financial Advisor (Mali Müşavir) to ensure every last bit of income and every expense for the year is recorded, all your accounts are reconciled, and any final adjustments are made. They will use these finalised figures to prepare your corporate or income tax returns.

It’s also the perfect time to analyse your performance over the year. Generate your key financial reports, like the Profit & Loss statement and the Balance Sheet. These documents give you a powerful, high-level overview of your profitability and overall financial standing over the last twelve months.

Finally, knowing the key tax deadlines is crucial for avoiding costly penalties. While your advisor will handle the actual submissions, it’s ultimately your responsibility to provide them with complete and accurate information on time.

To help you stay on track, here’s a quick summary of the most important recurring deadlines that small and medium-sized enterprises (SMEs) in Turkey need to watch out for.

Key Turkish Tax Declaration and Payment Deadlines for SMEs

Tax Type

Declaration Frequency

Typical Deadline

Value Added Tax (KDV)

Monthly

By the 28th of the following month

Withholding Tax (Stopaj)

Quarterly

By the 26th of the month after the quarter ends

Advance Corporate/Income Tax

Quarterly

By the 17th of the second month after the quarter ends

Annual Corporate/Income Tax

Annually

By the end of April (Corporate) or March (Income)

Having these dates on your calendar helps you plan ahead and ensures you and your advisor have plenty of time to get everything filed correctly, keeping you in good standing with the tax authorities.

When and How to Hire a Financial Advisor

Why invoices, records, and compliance require a certified Mali Müşavir

While the right bookkeeping software gives you a powerful command centre for your daily finances, there comes a point where automation just isn’t enough. In Turkey, navigating the complex web of tax law and corporate regulations is absolutely not a DIY project.

Hiring a professional isn’t just a smart move; in most cases, it’s a legal necessity. This is where the Mali Müşavir comes in.

This title translates to Financial Advisor or Certified Public Accountant, but they are far more than just someone who helps at tax time. They are your legally mandated partner in compliance, handling crucial tasks that a business owner is simply not permitted to do alone.

The Non-Negotiable Role of a Mali Müşavir

Let’s be perfectly clear: under Turkish law, you cannot submit your company’s official tax declarations yourself. Things like your monthly KDV (VAT) returns or your annual corporate tax filings must be prepared, signed, and submitted by a certified Mali Müşavir who holds a professional licence.

Attempting to sidestep this is a non-starter. Your company’s good standing with the Turkish Revenue Administration (GİB) hinges entirely on having a certified professional manage these official submissions. They are the essential bridge between your books and the government.

Their job goes way beyond just filing paperwork. A great advisor will:

Structure your chart of accounts to be fully compliant with Turkish standards.

Oversee your entire year-end closing process for complete accuracy.

Represent you during a tax audit, acting as your professional line of defence.

Offer genuinely useful strategic advice on tax planning and financial efficiency.

Finding and Vetting the Right Advisor

Finding the right Mali Müşavir is one of the most important decisions you’ll make for your business’s financial health. The industry is huge—the broader Accounting & Auditing sector in Turkey, which serves small businesses, is made up of around 57,556 businesses. It’s also an industry in transition, moving from old-school service models to more modern, tech-integrated approaches. You can get more industry context from this ibisworld.com report on Turkish accounting.

I always suggest starting your search with personal referrals from other business owners in your network. Look specifically for advisors who are comfortable with modern cloud-based software, as this makes collaboration so much smoother.

Before you sign anything, have a detailed conversation. This is a long-term partnership, so you need to be sure they’re the right fit. For more on this, you might find our guide on what to know before seeking consulting services in Turkey helpful.

Key Questions to Ask Before You Hire

When you meet with potential advisors, treat it like a proper interview. After all, you’re entrusting them with the financial integrity of your entire business.

What bookkeeping software do you specialise in? You need an advisor who already knows your software, whether it’s Paraşüt, Logo, or something else. This avoids headaches and ensures they can access your data seamlessly.

How do you prefer to communicate? Are they an email person, or do they use a messaging app? Setting clear communication expectations prevents a lot of frustration down the road.

What, exactly, is included in your monthly fee? Ask for a detailed breakdown. Does the fee cover all mandatory filings and basic consultations, or are some things billed as extras? Nailing this down prevents surprise invoices.

Do you have experience with other businesses in my industry? An advisor who understands the specific financial quirks of your sector—be it e-commerce, consulting, or manufacturing—can offer far more valuable strategic advice.

Typical monthly retainer fees for a Mali Müşavir for a small business in Turkey can run from 1,500 TRY to 5,000 TRY or more, depending on your transaction volume and business complexity. See this as an investment. It buys you more than compliance; it buys you peace of mind and expert guidance, freeing you up to focus on what really matters: growing your business.

Common Questions About Turkish Bookkeeping

When you’re getting a business off the ground in Turkey, it’s the practical, everyday questions that often cause the most stress. Let’s cut through the confusion and tackle a few of the most common queries I hear from entrepreneurs. Getting these right from the start can save you a world of headaches down the road.

These aren’t just minor details; they’re the foundation of good financial management. Understanding them turns confusing rules into confident, daily habits, which is exactly what you need to keep your business healthy and compliant.

Can I Do My Own Bookkeeping as a Foreigner?

This is probably the question I get asked most, and the answer is a classic “yes, but…”

You can absolutely manage your day-to-day financial records—what we call “pre-accounting” or ön muhasebe. In fact, you should! Using good accounting software lets you handle your own invoicing, track every expense as it happens, and keep a close eye on your cash flow. This is your business’s financial pulse, and you need to have your finger on it.

The “but” comes in with official submissions. Turkish law is crystal clear on this: all official tax declarations and year-end financial statements must be signed and submitted by a certified Financial Advisor, known as a Mali Müşavir. You are legally required to have a licensed professional on record who handles this for you with the Turkish Revenue Administration (GİB).

So, the best approach is a partnership. You manage the daily ins and outs, and your advisor ensures everything is filed correctly and on time.

What Are the Biggest Bookkeeping Mistakes to Avoid?

I’ve seen a few common missteps trip up even the smartest business owners. If you can steer clear of these, you’ll be ahead of the game.

Mixing Personal and Business Finances. This is the cardinal sin of small business bookkeeping. Open a separate business bank account from day one. It’s not just good practice; it’s essential for clean records and makes any potential tax audit infinitely less painful.

Forgetting to Invoice Every Single Sale. In Turkey, an official invoice (e-fatura or e-arşiv) isn’t optional—it’s required for every transaction. That little cash sale you made? It needs an invoice. Failing to issue one is a serious compliance violation.

Missing Tax Deadlines. The dates for filing monthly VAT (KDV) and quarterly withholding tax (Stopaj) are non-negotiable. Missing them triggers automatic penalties. Put them in your calendar with multiple reminders.

Getting VAT Calculations Wrong. Turkey has several VAT rates, and applying the wrong one is a common error. This can lead to you overpaying or underpaying tax, both of which create messy problems to fix later. This is where good software really proves its worth.

Honestly, avoiding these problems comes down to building solid habits. Use that dedicated business account, issue an invoice the moment a sale is made, and trust your software and advisor to keep you on top of deadlines. It’s all about creating a system that makes doing the right thing the easiest option.

Do I Really Need to Keep All My Physical Receipts?

The answer has become a bit more nuanced with Turkey’s big push for digitalization (e-dönüşüm), but the core principle is simple: you must keep the legal original of every document.

Here’s what that means in practice:

For E-Invoices (e-Fatura/e-Arşiv): When you receive an invoice electronically through the official GİB portal, that digital file is the legal original. You don’t need to print it. Your responsibility is to store that electronic file securely for the mandatory 10-year period.

For Paper Invoices and Receipts: If a supplier hands you a traditional paper receipt, that piece of paper is the legally binding document. You are required to keep that physical copy safe for 10 years.

My advice? Scan all your paper documents and attach them to the transaction in your bookkeeping software. It’s a fantastic way to stay organised and have a digital backup. But remember, for paper documents, the scan is just a copy. If a tax inspector comes calling, they’ll want to see the original paper.

Navigating these financial and legal requirements is exactly what we do at Workon. We manage the complexities of Turkish business regulations—from setting up your company to handling all your ongoing compliance—so you can concentrate on what you do best. Let our team of experts give you the foundation you need to thrive. Find out more about our services.

Bookkeeping for sole proprietorships in Turkey is simpler, often single-entry. LLCs, however, require double-entry systems and official commercial books per Turkish law.

Yes. Turkish law requires all official tax declarations to be filed by a certified Financial Advisor (Mali Müşavir). Businesses cannot submit returns independently.

Key tax deadlines include monthly KDV (VAT) by the 28th, quarterly Stopaj (withholding tax) by the 26th, and annual corporate or income tax filings by April or March.

Top local options like Paraşüt, Logo İşbaşı, and MikroX offer direct integration with the Turkish Revenue Administration (GİB) and full e-Fatura\/e-Arşiv compliance.

Yes—foreigners can handle daily records and invoicing. However, all official filings must go through a licensed Mali Müşavir to remain legally compliant.

Subscribe to Newsletter

Be notified of the latest news in the business world quickly